Merrill Lynch Reprot

Essay by 24 • April 25, 2011 • 4,516 Words (19 Pages) • 1,395 Views

Essay Preview: Merrill Lynch Reprot

Merrill Lynch does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may

have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their

investment decision.

Refer to important disclosures on page 10 to 11. 10570583

GEM and FX Strategy

The coming correction in

global imbalances

The "central, global financial irony of our times" is Ð'...

Ð'... poor countries, needing capital to finance development, are sending large

amounts of money to rich countries such as the US on an unprecedented scale.

This global imbalance will start to reverse in 2007 ...

Ð'... via US slowdown, a decline in global savings and an increase in the supply of

non-US financial assets, with implications for the USD and emerging markets.

The US dollar is likely to weaken Ð'...

Ð'... particularly against currencies that are large providers of global capital, notably

the Chinese renmimbi, the Japanese yen and the Russian ruble.

EM bull market switches toward domestic demand themes Ð'...

Ð'... as emerging economies spend their savings to fund strong domestic economic

activity (Chart 1).

EM capital markets boom Ð'...

Ð'... as M&A activity, issuance and leverage in under-capitalized EM assets in real

estate, consumer and infrastructure sectors continue to escalate.

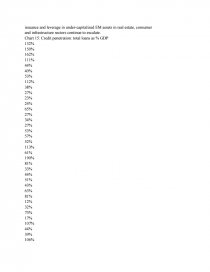

Chart 1: Current account surplus in EM & DM

Current account balance, US$bn

-800

-600

-400

-200

0

200

400

600

800

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006e 2007e

Emerging

Dev eloped

Source: Merrill Lynch estimates

Investment Strategy

Emerging Markets | Global

08 January 2007

Michael Hartnett +1 212 449 3600

Global EM Equity Strategist

MLPF&S

michael_hartnett@ml.com

Alex Patelis +44 20 7996 5897

Global FX Strategist

MLPF&S (UK)

alex_patelis@ml.com

GEM and FX Strategy

08 January 2007

2

Resilient global growth in 2007

Despite a significant slowdown in US growth this year, the ML Global Economics

team expects the global economy to weather the storm better than expected1. In

aggregate, we expect global growth ex-US to slow to 5.3% in 2007 from 5.8% in

2006, even as US growth slows to 1.7% from 3.2% (Chart 2).

There are five main reasons why we expect this global slowdown to be different

to the 2000-2001 experience:

A soft landing, not a recession, is the US base case. US consumption is not

expected to contract in coming quarters, as house price inflation decelerates,

but household wealth has been buttressed by resilient equity prices. Our US

economics group expects consumption growth to reach a low of 1.1%

annualized in 3Q07.

The world does not have direct exposure to the US housing sector. In

contrast to the 2000-01 tech implosion, there is little direct ownership of US

residential property by non-US individuals, little direct exposure of non-US

construction companies on US construction and limited direct exposure of

non-US financial companies to US mortgage debt.

The global economy is very robust; global growth over the past years has

been the strongest in recorded economic history. As such, this is an optimal

time for the global economy to be hit by a shock.

Global monetary policy has not tightened as much as in the US. The Fed has

raised its Fed funds target rate by a cumulative 425bp from its low, whereas

the Bank of Japan has raised its rate by just 25bp.

Our economists identify regional structural stories, such as prolonged

investment booms in Japan, Europe and many emerging markets, such as

India. High profitability, a low cost of capital, low levels of debt, high cash

levels and high productivity growth all augur well for these developments

(Charts 3 & 4).

1

As outlined in "2007: The global macro year ahead," ML Global Economics, 29 November 2006.

Chart 2: US growth and non-US global growth

Source:

...

...